Launch / Digital banking / Credit cards / 2006-present

Tinkoff Trust Case

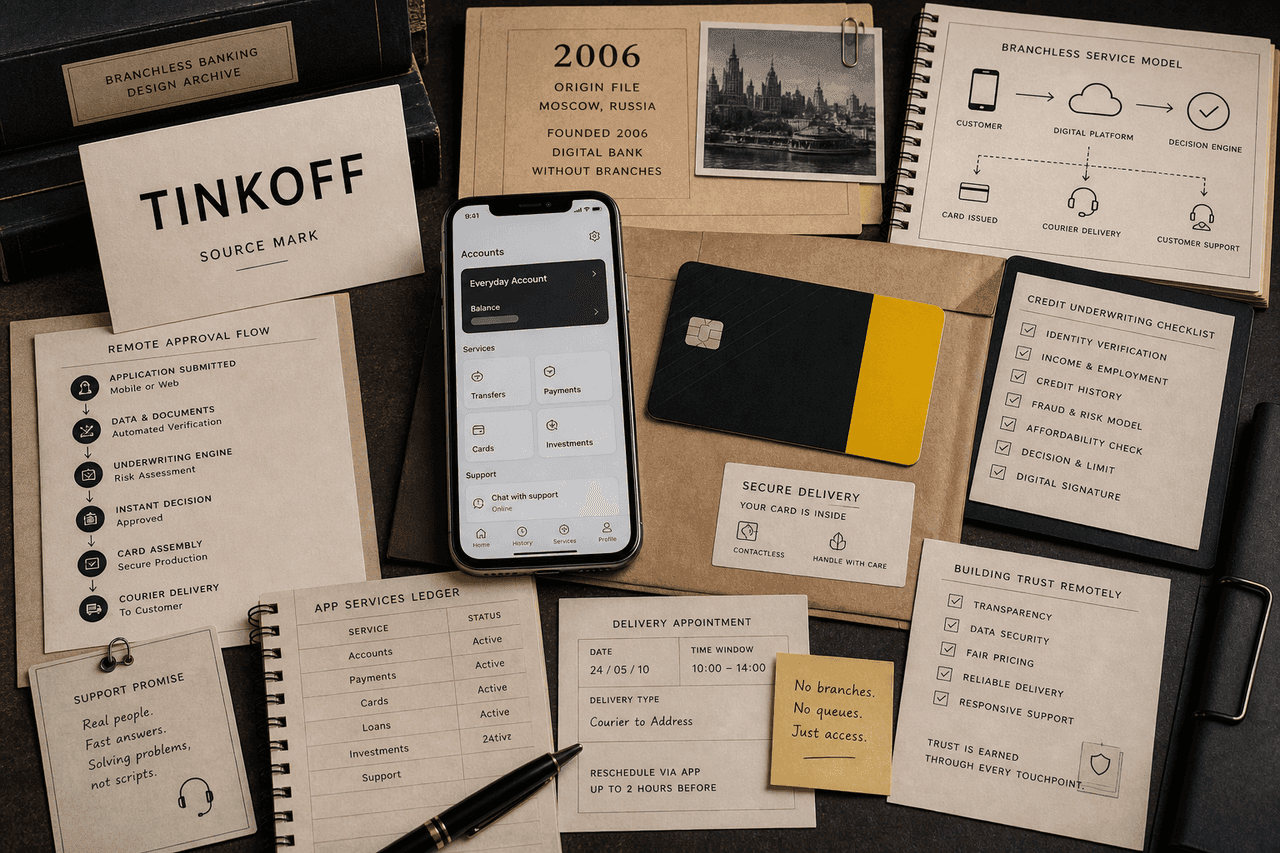

Tinkoff made branchless banking feel usable by joining remote application, card delivery, app service, underwriting flow, customer support, and credit access without a branch visit.

Short Answer

Tinkoff Trust Case is a launch case about Tinkoff in 2006-present. Tinkoff made bank trust work without the branch. Branchless banking needs a replacement for the old trust ritual. Tinkoff used application flow, card delivery, app service, and support to make remote finance read real.

Reader Task

What this entry should help you finish

Use this entry to finish four jobs: answer what happened to Tinkoff, see why it belongs in the launch lane, inspect the decision consequence, and leave with the operator lesson. The point is not to remember the brand. The point is to know what decision, proof surface, or failure mode a team should check next. Then compare it with Nubank, Monzo, iFood before turning the case into a rule.

What Tinkoff teaches

- Tinkoff traces its origin to 2006.

- The brand is associated with branchless banking, cards, app service, and remote delivery.

- Grow Your Brand value is bank trust rebuilt through workflow instead of branch presence.

- The operator lesson is to replace the old trust ritual before removing it.

Why This Brand Belongs In Grow Your Brand

Tinkoff belongs in Grow Your Brand because the page studies a specific brand decision, not a company profile. The decision sits in launch and gives operators a way to see how trust changes commercial value.

The useful archive question is what changed in recognition, trust, demand, pricing power, category position, or public memory after the market saw the move.

The Brand Asset At Stake

The asset at stake is access, transaction confidence, service recovery, and visible risk control. That asset matters because it affects how people find, understand, choose, trust, or repeat the brand when the company is not in the room to explain itself.

For Tinkoff, the asset is not abstract equity. It has to show up in the buying surface, product surface, service route, source record, or repeated customer behavior.

What Changed

Tinkoff made bank trust work without the branch.

The change forced the market to decide whether the old shortcut still worked, whether the new proof was strong enough, and whether the brand had made the category easier or harder to understand.

What The Market Learned

The market learned to judge Tinkoff through the gap between the visible move and the proof behind it. calling the brand trusted while avoiding the proof of access, error handling, fees, service, and recovery is the weak reading this page is meant to prevent.

A useful brand decision makes buying, remembering, trusting, or repeating easier. A weak decision makes the audience do more work before it believes the claim.

Commercial Consequence

The commercial consequence sits in trust: access, transaction confidence, service recovery, and visible risk control. When that proof becomes easier to see, customers have more reason to choose, trust, repeat, or pay attention. When it becomes harder to see, the brand has to spend more money explaining what the market used to understand faster.

Tinkoff matters because the decision changed more than presentation. It changed buyer confidence, memory, category position, or repeat behavior in digital banking / credit cards. That is why the case belongs in a brand decision library instead of a general company profile.

What Another Brand Should Learn

Another brand should use this case before spending money on a similar move. Name the customer behavior, the proof surface, the protected cue, and the consequence that would make the decision worth the cost.

If the same proof does not exist in the business, copying Tinkoff would copy the surface while missing the reason the decision mattered.

The Decision Context

A branchless bank removes a familiar proof point. The customer no longer walks into a building to make the service feel real.

Tinkoff's system had to replace that with approval flow, delivery, app service, and support.

Delivery Made The Bank Physical

The card handoff matters because it turns a remote decision into a concrete object.

That made the branchless model easier to trust.

The Signal Reading

Tinkoff belongs in Grow Your Brand because it shows how banking can move trust from place to process.

For operators, the lesson is to design the replacement ritual before cutting the old one away.

Where The Strategy Can Break

Tinkoff should not be read as a clean success label. The useful question is where the launch promise can fail in the real category: customers are being asked to place money, identity, credit, or protection inside the system.

The weak reading is calling the brand trusted while avoiding the proof of access, error handling, fees, service, and recovery. That kind of page sounds polished but gives the reader no way to judge the decision.

The concrete failure mode is this: the public remembers the friction point first: a blocked account, a confusing fee, a failed claim, a poor branch handoff, or a weak digital recovery path. If the case cannot explain that risk, the brand story is not finished.

The Bad Example

A bad Tinkoff copycat would start with the visible surface: the mark, the color, the store, the app, the route, the campaign, or the public phrase. Then it would assume the surface created the result.

That is usually backwards. The surface worked only if the category proof underneath it was already strong enough: access, transaction confidence, service recovery, and visible risk control.

The page has to protect readers from that shortcut. The mistake is not ambition. The mistake is copying the artifact while leaving the constraint untouched.

What To Copy

Copy the discipline, not the costume. For Tinkoff, the discipline sits in the link between digital banking / credit cards pressure, customer behavior, and the proof a buyer or user can inspect.

A useful reader should be able to point to one behavior that changed, one risk that dropped, and one cue that helped the change stick.

If those three pieces are missing, the page should not pretend the case is a repeatable playbook. It is only a brand example with missing machinery.

The Proof Trail

Start with the year or period: 2006-present. Then ask what was visible to the market at that time, what changed after the decision, and what evidence still exists now.

The source list gives the inspection trail. Use it to separate what Tinkoff says about itself from what the case page argues about the brand decision.

The proof should answer five checks: money or protection risk, access proof, service recovery, fee or claim clarity, regulatory and trust burden. If the page cannot answer them, the case needs more source work before anyone treats it as a decision record.

The Decision Limit

The case should not be used as a slogan for doing the same thing. It should be used as a boundary test. The question is whether the same market pressure, customer behavior, proof surface, and timing exist before the decision gets copied.

Tinkoff gives Grow Your Brand a concrete inspection point: access, transaction confidence, service recovery, and visible risk control. If a team cannot point to that proof in its own business, the comparison is weak, even when the visible asset looks similar.

The better lesson is operational. Decide what must be true before the cue, campaign, name, product, route, or experience can carry the promise. Then decide which signal would stop the move if customers reject it, ignore it, or use it in the wrong way.

A serious reader should leave with a constraint, not a mood. For Tinkoff, the constraint sits in digital banking / credit cards: who is choosing, what risk they are managing, which proof they can inspect, and what would make the promise collapse under normal use.

The final check is the comparison set. Put Tinkoff beside two adjacent cases and ask what changed in each file: the cue, the behavior, the channel, the proof, the public language, or the operating burden. The answer keeps the case from becoming trivia.

This is where Grow Your Brand page earns its keep. It turns a brand story into a decision memo: what changed, who had to believe it, what proof reduced the risk, what failure would expose the gap, and which nearby cases warn against copying the surface too quickly.

Compare Next

Related Cases

Do not read Tinkoff alone. Compare it against nearby cases: Nubank, Monzo, iFood.

Sources

{kind=link}

People Also Ask

What happened to Tinkoff?

Tinkoff Trust Case is a launch case about Tinkoff in 2006-present. Tinkoff made bank trust work without the branch. Branchless banking needs a replacement for the old trust ritual. Tinkoff used application flow, card delivery, app service, and support to make remote finance read real.

Why is Tinkoff a launch case?

Tinkoff is filed as a launch case because the visible consequence sits in that decision pattern. Tinkoff made bank trust work without the branch.

What can brands learn from Tinkoff?

Branchless banking needs a replacement for the old trust ritual. Tinkoff used application flow, card delivery, app service, and support to make remote finance feel real.

Is Tinkoff still operating?

Grow Your Brand marks Tinkoff as Active / continuing. That means the brand, company, platform, product system, or parent organization is still operating, continuing, or being actively resolved.

What should Tinkoff be compared with?

Compare Tinkoff with Nubank, Monzo, iFood to see the same decision pattern from nearby cases.